THIS MATERIAL IS A MARKETING COMMUNICATION.

Tesla – All Eyes on China

Tesla is now the most valuable car company in the world by market capitalization, overtaking Toyota despite only being projected to sell less than 5% of the latter’s volume for 2020 and accounting for less than 1% of global volume. Tesla is seen as a key disruptor in the auto space stemming from its focused all-BEV strategy without the need to protect the profitability of a legacy ICE business, as well as an innovator in battery technology and a pioneer in autonomous driving.

More importantly, Tesla has demonstrated a legitimate pathway to profitability for EV start-ups and has successfully overcome teething execution and ramp up issues. The market expects Tesla to continue gaining market share in the premium auto space and further penetrate into the Chinese market. As Tesla looks to extend its leadership in battery technology and further lower its cost base to remain competitive, we believe that setting up a factory in China will allow Tesla to be closer to its supply chain and fully tap onto the capabilities of China’s burgeoning EV supply chain.

Tesla’s Shanghai factory is the company’s first car manufacturing site outside the USA and key to Elon Musk’s ambition of boosting sales in the world’s largest auto market while avoiding high import tariffs on US made cars. The new factory (Gigafactory 3) is also the first fully foreign owned auto manufacturing plant in China. Tesla will mainly produce the Model 3 (sedan) and Model Y (compact SUV) for the Chinese market. Tesla’s Model 3 was the top selling plug-in car in 2019 with close to 14% market share according to Insideevs.com. The aim is to ramp up production to as many as 500k vehicles per year in two to three years’ time. As around 70% of Tesla’s components for production in China are still sourced from overseas, it makes sense to localize production in order to improve margins or lower ASP, depending on the strategy Tesla chooses in China.

Tesla's Timeline in China

- Oct 2018 - Tesla attained the right to use 1,200 acres of land in Shanghai Lingang from Shanghai government with total Rmb973mn, which used for Tesla's first Gigafactory outside the U.S.

- Jan 2019 - Tesla held the groundbreaking ceremony of the Gigafactory and started the construction.

- Aug 2019 - Tesla's Shanghai Gigafactory was granted the first comprehensive acceptance certification.

- Sep 2019 - Tesla's Shanghai Gigafactory passed the second government acceptance check.

- Oct 2019 - Tesla's Shanghai Gigafactory received the manufacturing certification and started the production of Model 3.

- Dec 2019 - The China-made Model 3 Sedans was officially delivered in Shanghai Gigafactory to its employee customers.

- Jan 2020 - The China-made Model 3 Sedans was officially delivered to its customers; Tesla started the manufacturing of Model Y.

China further reduced subsidies for EVs by 10% in 2020 and made the lower subsidies only available to EVs that cost less than Rmb300k. This caused Tesla to cut the starting price of the base model of its China made Model 3 to below Rmb300k in order to qualify for the subsidies. The company also cut the price of its longer range variant to offset the subsidy removal soon because the car would still cost more than the Rmb300k threshold required to qualify. This increases Tesla’s need to lower costs in order to maintain/improve margins.

According to Tesla’s manufacturing director of its Shanghai plant Song Gang in an interview with Bloomberg News, Tesla plans to increase local sourcing to 100% in China by the end of the year from the current 30%. We believe this will benefit the domestic supply chain in China from the import substitution trend. That said, expectations should be tempered given Tesla’s lower level of component outsourcing vs traditional ICE cars (with the majority of costs being allocated to battery makers) and Tesla’s still small production volume as a percentage of China’s total PV market (UBS forecasts Tesla’s 2020 production volume to account for just 0.5% of China’s PV volume and reach 2% based on Tesla’s three-year plan to produce 500k units a year).

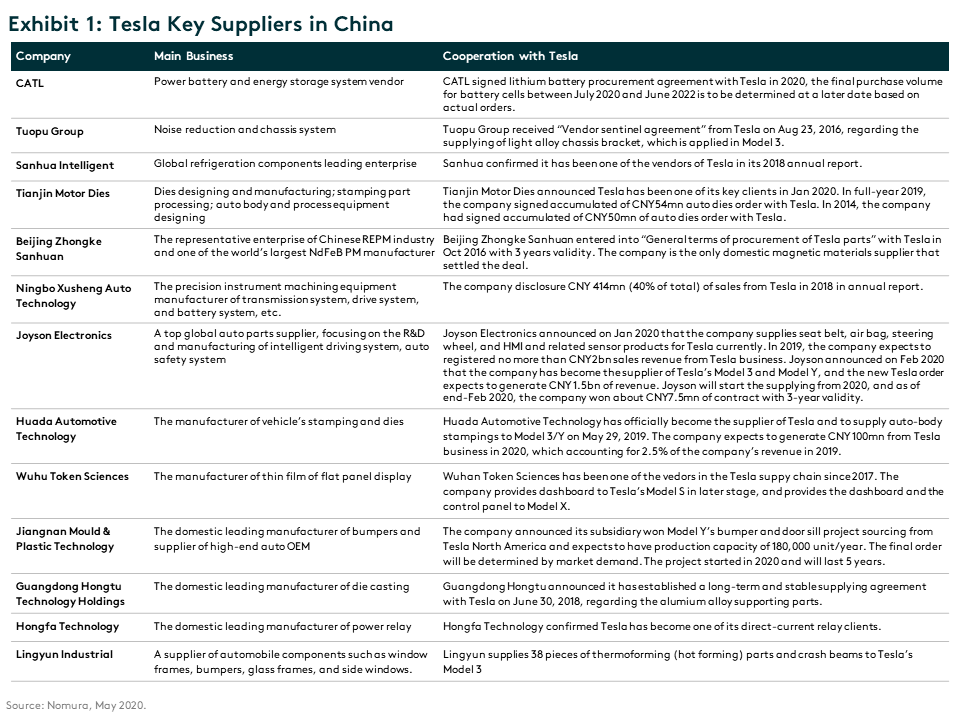

Some of the key suppliers to Tesla in China include CATL (EV battery and energy storage), Huayu (seats, large interior and exterior parts, clusters, central consoles, moldings etc), Joyson Electronics (seat belt, air bag, steering wheel, sensors), Huada Automotive (auto body stampings), Wuhu Token Sciences (dashboard), Sanhua Intelligent (HVAC), Hongfa Technology (direct-current relay), Guangdong Hongtu Technology (aluminum alloy support parts) etc.

If China’s EV supply chain is able to meet Tesla’s stringent requirements on quality and cost, we believe this will help to further boost the credibility of the Chinese companies and persuade more global OEMs to give these companies a shot. With more orders, Chinese companies in the EV value chain will be given opportunities to improve their technology with more funding and reduce costs through economies of scale. This will ultimately elevate the whole EV supply chain in China and is a win-win situation for the Chinese government, EV suppliers and OEMs.

1 CNBC, as of 1 July.

2 Inside EV.

3 UBS.

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KIIDs”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KIIDs can be obtained from www.am.miraeasset.eu/fund-literature/ . The Prospectus is available in English, French, German, and Danish, while the KIIDs are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KIID before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary/.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Hong Kong: This document is intended for Hong Kong investors. Before making any investment decision to invest in the Fund, Investors should read the Fund’s Prospectus and the information for Hong Kong investors (of applicable) of the Fund for details and the risk factors. The individual and Mirae Asset Global Investments (Hong Kong) Limited may hold the individual securities mentioned. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Copyright 2025. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.