THIS MATERIAL IS A MARKETING COMMUNICATION.

Lens into the Chinese Laser Industry

Since the invention of laser over 50 years ago, the technology has revolutionized to a broad range of applications and products across industries. The laser industry now has a complete and mature industry chain layout, including upstream laser materials and supporting components, the midstream laser beam sources and laser equipment and systems, as well as various downstream laser applications and consumption products across a broad range of industries.

This article will provide a synopsis on the laser industry in China through understanding:

- Development of Industrial Lasers,

- Our View of this Sector in China, and

- the ESG Benefits of Laser Technology.

Development of Industrial Laser Technology

Lasers provide flexible, non-contact, and high-speed ways to process and treat various materials, and are a key enabler of advanced manufacturing techniques, including automation and miniaturization. Therefore, industrial laser systems are continuously gaining share in the materials processing market within the automotive, aerospace, energy, electronics, consumer appliances, and heavy machinery sectors.

The integration of laser with other automation technologies, such as robotics and vision, enables new applications and enhances the utility of laser technology. Advances in laser and automation technologies reinforce each other. The speed and precision of laser processing are determined by not only the laser source, but also by the robot and machine tool it is integrated with. In high-power applications, thermal impact challenges motion control precision and stability and needs to be compensated for with advanced automation technologies. In other cases, sophisticated and novel motion control enhances laser material processing quality and expands its scope with the same laser source.

Our View

We believe that laser will consistently displace and outgrow conventional material processing technologies and become a crucial tool in factory automation. Fiber laser is the most important industrial laser type and should continue to take share from legacy types such as gas and solid-state lasers. By industry, the automotive industry is the largest customer, with the laser being used to make the car body and power train. Together with consumer electronics, these two sectors account for the bulk of demand, although other usages like welding, micromachining, and additive manufacturing are growing faster. In particular, the increasing complexity of the Apple iPhone in terms of functions and components involves more laser precision due to the form factor and a denser PCB (Printed Circuit Board). The miniaturization trend of the PCB drives adoption for more laser welding and drilling because of its higher precision in laser micromachining.

In particular, we believe that Hans Laser is a key beneficiary of iPhone model cycle changes. The company is the leading laser processing solution provider in China specializing in mobile devices such as smartphones, tablets and wearables. Key customers of Hans Laser for low-power laser (mostly smartphone related) include Apple, Huawei, Oppo and Vivo. The company also supplies to BOE Tech for LCD devices, Shengyi Tech and Kinwong Electronic in the PCB sector and CATL in the Electronic Vehicle (EV) space.

During the past few years, China has been the key driver of the global industrial laser equipment market with a remarkable Compound Annual Growth Rate (CAGR1) of 26.1% in 2011-17, far above the 11% CAGR of the global market. As of 2017, China accounted for approximately 43% of the global industrial laser equipment market, up from 18% as of 2010. In particular, China, as the major manufacturing base of the world, is considered to be the largest market for laser marking and metal cutting systems, while East Asia (Japan and South Korea) is the largest market for laser micro-processing and laser semiconductor processing equipment. The industrial laser market in China is expected to be impacted this year by the pandemic, though we should see a resumption of growth in 2021.

The outperformance of the China industrial laser market is also evidenced by the growing contribution of the market in the revenue mix of IPG Photonics Co. (“IPG”2), the global leader in high-power fiber lasers, the most popular laser solutions in general manufacturing industrials. IPG registered a CAGR of 24.8% in total revenue in 2011-17, within which, China delivered a CAGR of 40.4%, with revenue contribution rising to 44% as of 2017, up from 19% as of 2010. However, the trade war has had a widespread impact on investment decisions of general manufacturers in China since 2H18, in addition to the down-cycle of consumer electronics. These are two major downstream demand sources for China’s industrial laser equipment.

As at November 2019, fiber lasers have now become the main laser source for material processing in China, accounting for more than 60%3 of the laser processing market. The positive effect of the laser price reduction is the rapid spread of applications where prices are sensitive to end users, especially in metal cutting, marking, and cleaning. In 2018, 30,000 units of mid-power and 6000 units of high-power laser cutting systems, as well as 130,000 units of laser markers, were sold in China.

According to the Annual Report on the China Laser Industry, as of 2017, China’s low-power fiber laser source (<100W) localization rate reached approximately 93%, rapidly rising from 63% as of 2014. Meanwhile, the localization rates of mid/high-power fiber laser source (100W-1.5KW) and high-power fiber laser source (>1.5KW) rose to 63% and 10% as of 2017, from 17% and 1% as of 2013 respectively. Along this trajectory, we think there is significant room for domestic fiber lasers to further substitute the imported mid to high power fiber lasers going forward.

In our view, the key competitive advantages of Chinese fiber laser source makers include:

- Favorable Market Access - Chinese makers have favorable market access since China is a major manufacturing base in the world, as well as the largest market for laser marking and metal cutting systems with faster growing demand on laser applications

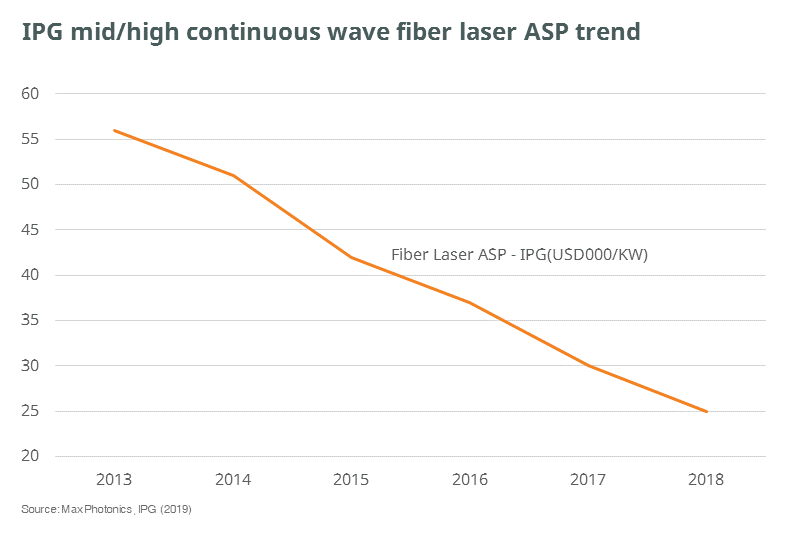

- Attractive Average Selling Price (ASP) - Chinese players have achieved an attractive ASP discount to foreign leading players such as IPG. IPG indicated a 17% CAGR of continuous wave (“CW”) fiber laser, ASP declined in 2015-18; while some Chinese fiber laser makers saw CAGR declined of approximately 25%. That said, the ASP gap of fiber lasers between Chinese players and IPG has been widening, thanks to both raw material unit cost savings and RMB/USD FX rate depreciation.

However, we believe in the next five to ten years IPG should be able to maintain its market position in the high-end fiber laser market. There is still a significant technology gap between IPG and Raycus, a leading Chinese fiber laser source maker. IPG has completed the R&D (Research & Development) for up to 120KW CW ytterbium fiber lasers and up to 20KW single-mode and low-mode output ytterbium fiber lasers. It has achieved the commercial production for 15-20KW CW fiber lasers, while seeing drastic sales expansion for 6KW and above CW fiber lasers in the cutting applications. That said, we believe Chinese fiber laser source makers, spearheaded by Raycus, have managed to narrow the gap with IPG and should continue to outperform in shipment volume in the near future by offering higher quality/price fiber lasers with elevating power levels.

ESG Benefits of Industrial Lasers

From an ESG perspective, there are significant positives using laser as compared to traditional manufacturing methods. Firstly, due to more concentrated energy delivery and much faster processing speed in cutting and welding, fiber laser saves 70-90% of total energy consumption compared to conventional methods, such as punch press and arc welding. Secondly, laser reduces the use of costly and hard-to-make physical templates, tooling, and supplements, therefore reducing the environmental footprint. Thirdly, thanks to its flexibility and precision, laser material processing is key in its technology in reducing waste and scrap, hence saving raw materials. Furthermore, laser also enables the use of innovative materials (e.g. aluminum, plastic, and composite) that are lighter and stronger, but difficult to process with legacy cutting and welding methods. Finally, laser replaces chemicals in marking and metal surface cleaning. It also saves hundreds of millions in tons of water used to treat these chemicals every year.

In conclusion, we believe there is still headroom for growth in the industrial laser industry in China. Although market share is still dominated by foreign players like IPG, many Chinese local players are catching up in their respective target markets and are expected to benefit from this growing sector.

1 CAGR is the rate of return that would be required for an investment to grow from its beginning balance to its ending balance, assuming the profits were reinvested at the end of each year of the investment’s lifespan.

2 This company was selected for illustrative purposes only of this fund marketing material. This is not a recommendation or advice to buy or sell any securities.

3 Source: The status of industrial lasers in China. https://www.industrial-lasers.com/home/article/14068621/the-status-of-industrial-lasers-in-china

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KIIDs”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KIIDs can be obtained from www.am.miraeasset.eu/fund-literature/ . The Prospectus is available in English, French, German, and Danish, while the KIIDs are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KIID before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary/.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Hong Kong: This document is intended for Hong Kong investors. Before making any investment decision to invest in the Fund, Investors should read the Fund’s Prospectus and the information for Hong Kong investors (of applicable) of the Fund for details and the risk factors. The individual and Mirae Asset Global Investments (Hong Kong) Limited may hold the individual securities mentioned. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Copyright 2025. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.