THIS MATERIAL IS A MARKETING COMMUNICATION.

Sun on the Horizon: the Middle East’s Solar Aspirations

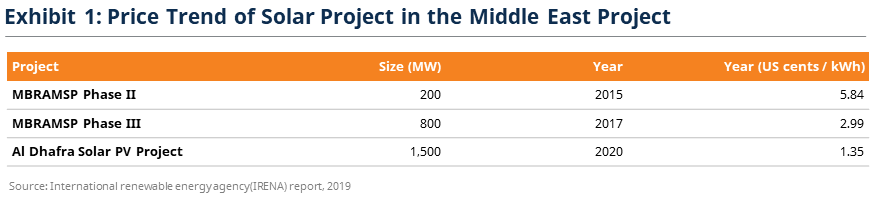

It was astonishing to see the world’s lowest tariff for a solar power plant in the Al Dhafra Region of the UAE recently. Abu Dhabi Power Corporation says it has received a bid of just 1.35 US cents per kilowatt-hour for the project, which is dramatically less than one-third of the projects built five years ago in the same area.

China overall accounts for over 70%1 of the module supply in the major solar projects of the Middle East region. As one of the world’s most attractive solar markets, the cost-competitiveness of the Al Dhafra Region, lowering the power costs and driving the demands, indicates that the upstream Chinese supply chain will be beneficial. In this article, we would like to explore the aggressive price strategy of the solar project in the Middle East region, its implications for other countries, and how China can benefit from these developments.

Low Cost, High Quality

The lowest levelized cost of energy (“LCOE”) in solar plant projects of the Middle East markets can be attributed to a number of key factors, including (1) top solar utilization hours in the world; and (2) low soft cost inland, financing, labor, and tax.

Top Solar Utilization Hours in the World

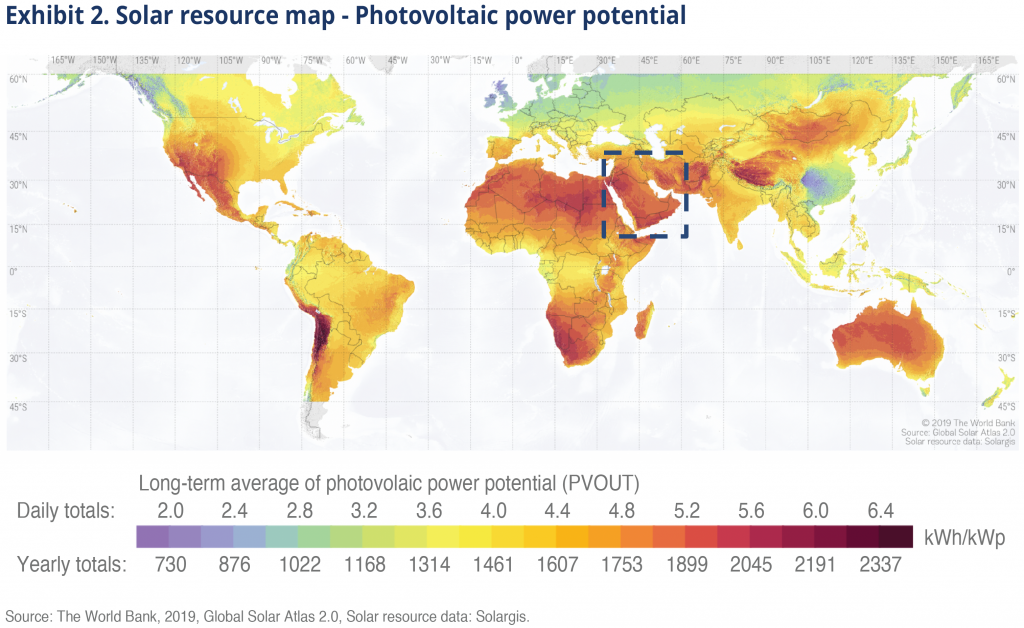

Citing Exhibit 1, the Middle East area is home to excellent solar resources, particularly in the Northwestern and Central regions of Saudi Arabia and the Southwestern part of Oman. The UAE, Bahrain, Kuwait, and Qatar also have excellent annual average irradiation. Currently, the UAE’s yearly irradiation can achieve 2,200 kWh per square meter, which is almost twice that of most of Europe and China east coastline, accordingly Exhibit 2. It helps with the lowest-cost solar LCOE without subsidies.

Soft-cost Benefits

Middle Eastern countries are not only blessed with substantial solar energy resources, but also have substantial land reserves to tap that resource. Large swathes of desert land with few trees or vegetation provide near-lossless solar radiation for solar modules, which allows authorities to plan some of the largest solar power projects in the world. In the UAE, for example, the Dubai Electricity & Water Authority has planned a 5 GW solar power park while the Abu Dhabi Electricity & Water Authority is working on a 1.17 GW solar power park.1 It appears that developers did not have to account for land costs that could be around US$5,000 per acre in the US, and the entire land-related cost could be 2/3 of the US1.

Moreover, Middle Eastern countries have reduced their lending rates sharply since the economic slowdown in 2008. The Saudi Arabian Monetary Authority reduced the lending rate from 5.5% to 2.0% in a matter of just four months between October 2008 and January 2009; the lending rate has remained constant at 2% since then. The UAE also cut interest rates during the 2008 financial crisis from 4.75% to 1% and maintained a low rate for a long time. As the market matures and regional commercial banks gain experience with renewable energy projects, debt conditions are becoming more attractive. As renewable energy in the region is generally receiving loans with long loan tenors over 20 years, high debt-to-equity ratios ranging between 70% and 86%, and low-interest rates between 120 and 200 bps plus libor2, which are very competitive with utility-scale solar projects being developed around the world.

The average hourly labor cost in manufacturing in the Middle East area is $5 vs. West and North Europe of $40+, the rest of Europe $10~20, North America $26, Australia $20, South America $1.8~6, China $5.4, India $3.4 and South-Eastern Asia $1.1~2.5.3 It is quite competitive against most areas in the world. What is more? Middle East countries offer tax discounts to attract solar project installation. For example, no sales tax is imposed on solar projects in the UAE vs. 5% in the US and UK.

Unique or Ordinary?

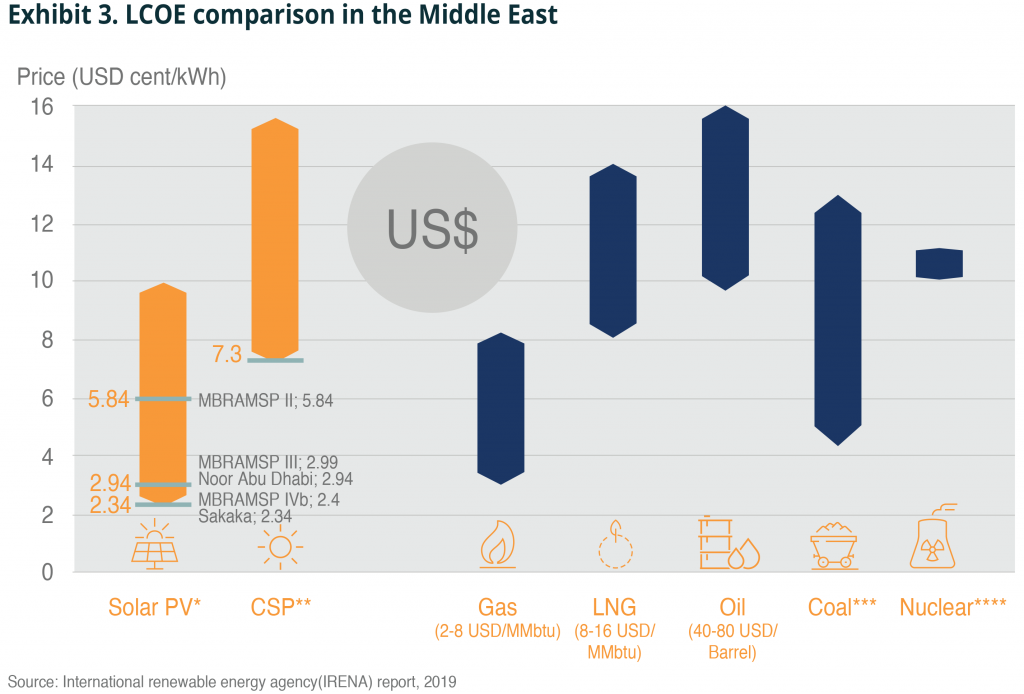

We could see from Exhibit 3 that photovoltaic projects are very competitive in the cost side, compared with electricity generation from oil, nuclear energy, and coal in the Middle East region. Solar energy has achieved customer side grid-parity in most places of the world and got cost side grid-parity in some areas with good solar resources or high power costs, such as India and Mexico.

Technology innovation pushes the module cost down fast in the past ten years, and it is expected to continue in the future. Citing Exhibit 1, the better the region is home to solar resources, the lower solar power cost it has with everything else the same. One example is Spain and Portugal, which are more active in solar installation than North Europe as the Iberian Peninsula has great solar irradiation. We expect the regions with yearly irradiation over 1,400 kWh per square meter4 are more likely first to achieve cost side grid-parity or accelerate solar installation. Some regions with good solar resources also have low-priced hydropower, such as South America and Australia; they have incentives to add solar farms, even not cost side grid parity.

Other than manufacturing cost, balance-of-system (“BoS”) cost accounts for the other half of the total cost, in which soft cost (land and financing cost) takes up a large percentage. Cutting soft costs will significantly help reduce LCOE. For example, commercial banks in China ask for an average 8% loan interest rate to fund a privately-owned solar farm, but only 4% for state-owned enterprises (“SOE”). Thus, the government is pushing SOEs to take over the existing solar farms, which will cut the financing cost by half, with everything remaining unchanged. Chinese central government and the solar industry are also talking about reducing the land cost, especially the wasteland that used to be of no value, but local government sells to solar farm operators for fiscal purposes.

Evolving Solar Ties between China and the Middle East

Being the world’s biggest manufacturer of photovoltaic products and dominating the solar equipment production of the Middle East, China takes advantage of the low-cost and high demands of the downstream developments in solar power. The cost-competitiveness of Abu Dhabi’s solar development is a push factor, driving the growth of the Chinese photovoltaic markets in the foreseeable future.

1 International renewable energy agency(IRENA) report, 2019.

2 International renewable energy agency(IRENA) report, 2019.

3 Trading Economics.

4 Mirae Asset Asia Pacific Research, June 2020.

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KIIDs”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KIIDs can be obtained from www.am.miraeasset.eu/fund-literature/ . The Prospectus is available in English, French, German, and Danish, while the KIIDs are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KIID before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary/.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Hong Kong: This document is intended for Hong Kong investors. Before making any investment decision to invest in the Fund, Investors should read the Fund’s Prospectus and the information for Hong Kong investors (of applicable) of the Fund for details and the risk factors. The individual and Mirae Asset Global Investments (Hong Kong) Limited may hold the individual securities mentioned. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Copyright 2025. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.