THIS MATERIAL IS A MARKETING COMMUNICATION.

The Trends that will Shape the Data Centre Market in 2020

The investment opportunities of the data centre markets in China continue to astonish many of us.

In this paper, we study the fundamentals of data centers, providing a deep dive into the various aspects of data centres in China, how they’re evolving and how investors can benefit from this driving force.

Fundamentals of Internet Data Centre (“IDC”)

Internet Data Centre – a physical facility where provides organizations with a centralized hub for storage, processing, management for a vast amount of data. The architectures of IDCs consist of electrical, cooling, and network infrastructure required to house large groups of servers and networking gear. The IDC operators own, manage, and lease out cabinets to customers (tenants) in these secured facilities, along with the power and cooling. Since IDCs play a crucial role in companies’ business continuity, covering various security devices, data communications, and interconnection services, they sit at the upstream ahead of cloud service solutions in the industry value chain (refer to below figure: Data Centre Industry Value Chain).

At the downstream of the data centre value chain, cloud services and solutions enable customers to put costly IT resources in public and private clouds, outsourcing services at the Infrastructure-as-a-Service (IaaS) level and procuring additional services at the Platform-as-a-Service (PaaS) and Software-as-a-Service (SaaS) layers.

IDCs consist of two main business models − the wholesale and retail colocation. Wholesale data centres are facilities where businesses with large footprint requirements, customizing specifications to fit the needs of customers and offering essential operational services such as physical security, uninterrupted power supply, and air conditioning.

For the retail colocation, operators lease individual standardized cabinets to tenants and host multiple customers within one data centre, offering basic operations along with value-added services such as IaaS, automation, and application managed services. Demand for wholesale data centre space is mainly steered by public cloud demand in China, with cloud service providers such as AliCloud, Tencent Cloud, Baidu Cloud, Huawei Cloud, Kingsoft Cloud, etc. being the major clients. On the other hand, the retail data centre market in China is structurally growing from private cloud demand, with enterprises and government entities driving the needs.

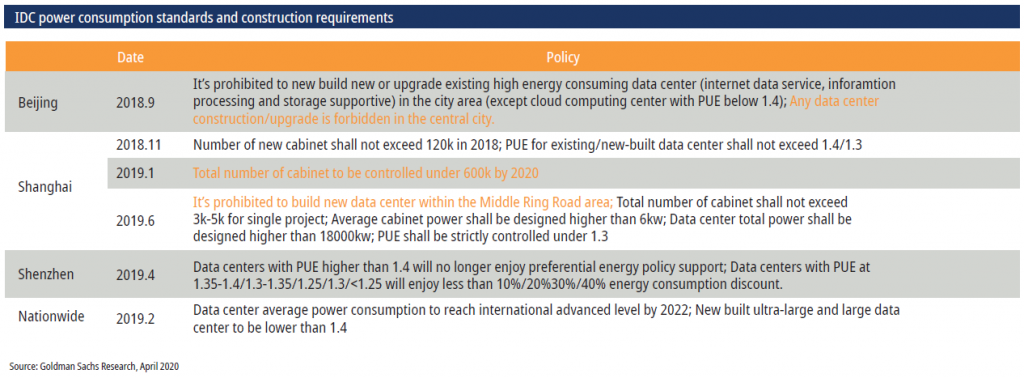

China’s Preferential and Control Policies Rolled Out

Data centres have been classified as new infrastructure by the Chinese government with a focus on accelerating the growth of this industry. As part of their fiscal stimulus package to speed up the COVID-19 recovery, the government is in discussions with industry leaders to spur the digital economy, by releasing more carbon quota, reducing power costs, and lowering financing costs for IDC operators.

The three major cities - Beijing, Shanghai, and Guangzhou, account for over two-thirds of data centre cabinet capacity in China, with utilization rates close to 80%.1 The choice of data centre hinges on customer proximity that customers prefer a data centre which has lower latency, higher utility reliability and is convenient in maintenance.

Due to the relatively high carbon emissions and power consumption of large scale IDCs, local governments in tier-one cities have stringent policy measures on the opening and expansion of new IDCs. In particular, both Beijing and Shanghai have prohibited new data centre projects in the cities. As a result, data centre operators are pushing their plans toward satellite cities, such as Langfang in Hebei province (55km from Beijing) and Kunshan in Jiangsu province (77km from Shanghai). We expect these cities will contribute to the considerable demands of data centres going forward.

Where Do Data Centres Go Next?

The total addressable market for China’s data centres is expected to grow at 26% CAGR from 2019-2023 to Rmb300bn2, thanks to the proliferation of mobile, gaming, and entertainment applications. The earlier adoption of 5G networks in China enables even more data-hungry applications from IoT to cloud computing to smart cities. Additionally, enterprises have increasingly moved their workloads to the data centres in a bid to leverage the new architecture, boosting the demand of IDA. With the world’s largest population, China has precipitated a move toward the big-data economy, and continued to enhance the data centre capabilities and evolves its growth to the next level.

China’s Leading Players

The three most significant Chinese players in IDC space – China Telecom, China Unicom, and China Mobile, are state-owned Telcos, which hold almost 50% of industry revenue. Independent carrier-neutral operators are fragmented to the rest of the market share.

Looking into the independent carrier-neutral operators, the largest neutral operator represents less than 5% market share. In spite of the low market share rate, we believe that carrier-neutral data centres have their competitive edges catering to fast-growing cloud/internet customers. Comparing to the cabinets of Telcos that are usually bulky and standardized, carrier-neutral IDCs are customized for the clients’ demands while offering a full suite of security and disaster recovery as well as quality customer services with dedicated personnel. Carrier-neutral IDCs tend to focus their buildout in data-hungry tier-one and adjacent cities where demand is more concentrated, translating into better pricing and superior returns. Carrier-neutral IDCs are not tied to one data service provider, offering diversity and flexibility for the client seeking services and allowing interconnection between different colocations and providers.

GDS, a leading brand for the carrier-neutral provider, dominates the market share of carrier-neutral IDC in China with premium assets in tier-one cities. With its aggressive rollout plan and high utilization rate, GDS has the highest revenue and EBITDA growth among peers.

21Vianet, the second-largest carrier-neutral IDC company in China, is seen as a catch-up play trading at a significant discount to the sector due to its weak operating track records in the past and a loss-making CDN and broadband business which hurt margins.

Sinnet is more focused on the retail business while having an established relationship with AWS, evidencing its robust capabilities. The company has the best ROIC in the industry, owing to higher asset turnover from the cloud business. Sinnet adopts a more prudent financial structure with low leverage compared to peers and high property ownership.

Backed by the Baosteel group, Baosight enjoys significantly lower rental and maintenance costs, benefitting by the parent company’s extensive networks and partnerships.

Your Gateway to Capture the Growing Opportunities of Chinese IDC

The Chinese IDC holds substantial investment opportunities. With the Chinese government speeding up the new infrastructure investment to combat economic pressure and boost sustainable growth, the country will be ahead of the curve in the next new ecosystem.

Global X China Cloud Computing ETF aims to track the performance of the Solactive China Cloud Computing Index NTR, representing the growth potential and resilience of companies that might position to benefit from the increased adoption of cloud computing technology in China. For investors looking to leverage the Chinese IDC long-term growth trajectory, Global X China Cloud Computing ETF may be the right choice.

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KIIDs”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KIIDs can be obtained from www.am.miraeasset.eu/fund-literature/ . The Prospectus is available in English, French, German, and Danish, while the KIIDs are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KIID before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary/.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Hong Kong: This document is intended for Hong Kong investors. Before making any investment decision to invest in the Fund, Investors should read the Fund’s Prospectus and the information for Hong Kong investors (of applicable) of the Fund for details and the risk factors. The individual and Mirae Asset Global Investments (Hong Kong) Limited may hold the individual securities mentioned. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Copyright 2025. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.