THIS MATERIAL IS A MARKETING COMMUNICATION.

Implications from UK’s Decision to Exit ICE by 2035

Implication from UK’s Decision to Exit Internal-Combustion-Engine (ICE) Cars by 2035

The UK government recently announced a plan to bring forward a complete ban on UK sales of petrol and diesel engine vehicles to 2035 from 2040. The decision was made in response to experts who said that 2040 was too late for the ban if the UK wanted to achieve its target of becoming net-zero by 2050. Contrary to industry expectations, the government is now including Hybrid Electric Vehicle (HEV) and Plug-in Hybrids Electric Vehicle (PHEV) in the ban. As cars are typically on UK roads for 14-15 years, a ban had to happen by 2035 to rid polluting vehicles from the road in time for net-zero emissions target of 2050.

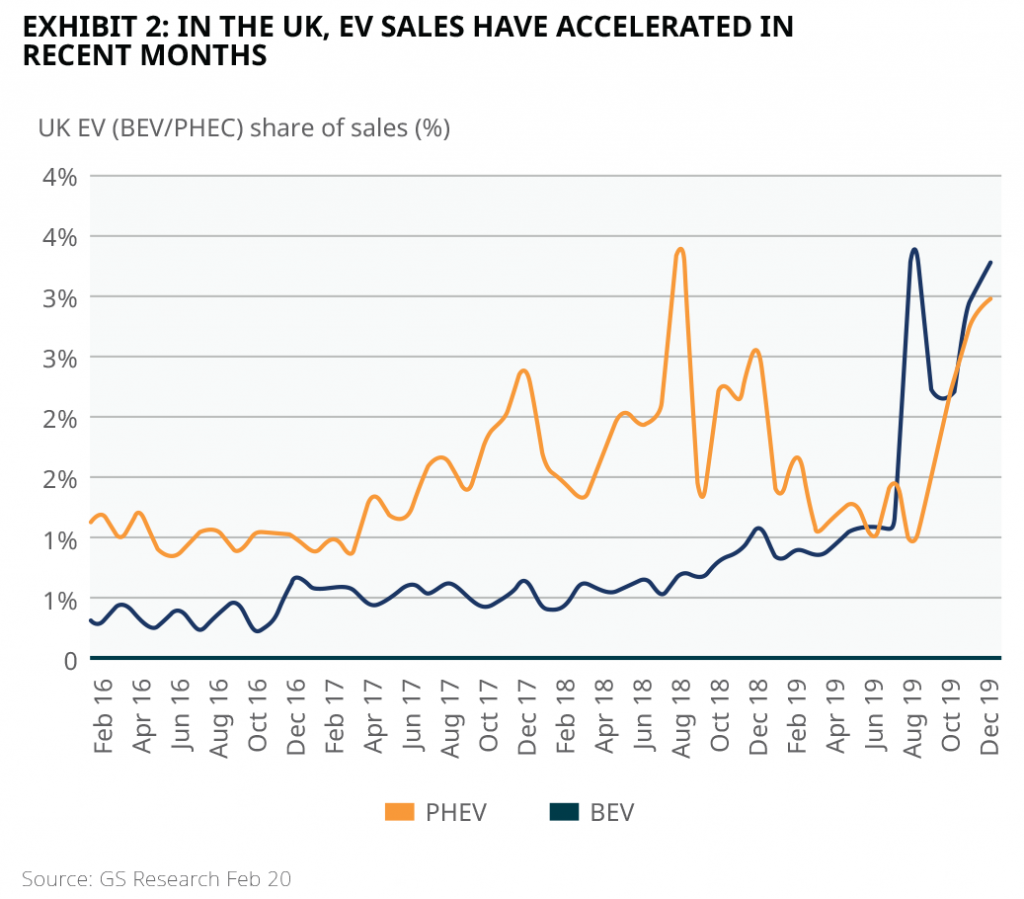

We believe the target to be exceedingly ambitious given the short period of time (less than two vehicle cycles; provided the vehicle development lead times are typically five years, and the subsequent life is 6-7 years) in addition to the current lack of charging infrastructure. To combat this, legal measures are being taken to create an open-access network of charging stations. 2035 regulations need to be taken into consideration by Original Equipment Manufacturers (OEMs) for their planning of next-generation products in the subsequent 1-2 years. The proposal is reportedly suggesting a stop-sale as opposed to a ban on vehicle usage by 2035. In the UK, currently, less than 3% of cars sold are Electric vehicle (EV), with Battery Electric Vehicle (BEV) only accounting for 1% of all cars sold. This would entail going from 1% to 100% in 15 years1. The situation will likely be exacerbated by Brexit, with imports into the UK likely to be more expensive than before due to tariffs. At the same time, the cost of making cars in the UK will also increase due to higher prices of imported auto components. To encourage the take-up of EVs and shorten waiting times for new vehicles, we think the UK government might encourage more direct OEM investment into UK-based supply chains such as battery giga-factories.

This latest proposal by the UK government seems more aggressive than what OEMs are projecting, mainly if PHEVs are included in the ban. Moreover, using the UK as an example, it would appear that the timeline is accelerating. The same could possibly happen in the EU. We believe that OEMs would no doubt have higher cost pressure as they plan for this expedited timeline, while the transition from ICE to BEVs would be even more painful than previously expected.

Among the OEMs, Volkswagen has a lead with respect to any expedited EV timeline. While most OEMs have BEV products in the market and plan to launch more in coming quarters, the level of VW’s spend (€33bn planned over five years) and ongoing strategy (2 dedicated BEV platforms, 8 dedicated MEB plants, 70+ new models by 2028) should see it well-placed to capitalise2. BMW’s BEV roll-out is less transparent than others, with only the MINI BEV, the iX3, i4, and iNext highlighted for launch. BMW continues to develop its BEVs on combined ICE/BEV platforms that are unlikely to maximize range and battery efficiency. The current specifications on the new electric MINI with a 32.6kWh battery and a 140-mile range are 35% less than the range that VW’s ID3 is offering. This does not suggest BMW is very keen to build a mass-volume BEV.

Among the OEMs, Volkswagen has a lead in terms of an expedited EV timeline. While most OEMs have BEV products in the market with plans to launch more in coming quarters, the level of VW’s spend (€33bn planned over five years) and ongoing strategy (2 dedicated BEV platforms, eight dedicated MEB plants, 70+ new models by 2028) should mean the company is well-placed to capitalise2. BMW’s BEV roll-out is less transparent than others, with only the MINI BEV, the iX3, i4, and iNext highlighted for launch. BMW continues to develop its BEVs on combined ICE/BEV platforms that are unlikely to maximize range and battery efficiency. The current specifications of the new electric MINI, 32.6kWh battery, and a 140-mile range is 35% less than the range of VW’s ID3.

Click here to download the full report.

Related ETFs:

•

Global X China Electric Vehicle ETF (2845 HKD / 9845 USD)

Footnotes

1 Source: Briefing Paper: Electric vehicles and infrastructure, UK Parliament, March 2020

2 Source: Volkswagen Company report, Nov 2019

3 Source: BMW Company report, Jan 2020

Disclaimer

This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service. The views and information discussed or referred in this document are as of the date of publication. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements.

Investment involves risk. Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (HK) Limited ("MAGIHK") are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

The document may contain information and material relating to funds that are authorized by the Securities and Futures Commission ("SFC") in Hong Kong. SFC authorization is not a recommendation or endorsement of a fund nor does it guarantee the commercial merits of a fund or its performance. It does not mean the fund is suitable for all investors nor is it an endorsement of its suitability for any particular investor or class of investors. The document is prepared by Mirae Asset Global Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Hong Kong: This material is prepared by Mirae Asset Global Investments (HK) Limited (Mirae HK). Mirae HK is regulated by the SFC (CE reference: ALK083).

Australia: The information contained on this document is provided by Mirae Asset Global Investments (HK) Limited ("MAGIHK"), which is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 (Cth) (Corporations Act) pursuant to ASIC Class Order 03/1103 (Class Order) in respect of the financial services it provides to wholesale clients (as defined in the Corporations Act) in Australia. MAGIHK is regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws, which differ from Australian laws. Pursuant to the Class Order, this document and any information regarding MAGIHK and its products is strictly provided to and intended for Australian wholesale clients only. By accessing this document and any information or content contained in it, you represent that you are a 'wholesale client' under the Corporations Act. This document is strictly for information purposes only and does not constitute a representation that any investment strategy is suitable or appropriate for an investor's individual circumstances. Further, this document should not be regarded by investors as a substitute for independent professional advice or the exercise of their own judgement. The contents of this document is prepared and maintained by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Australian Investments & Securities Commission. No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission of MAGI HK. Copyright 2020. All rights reserved.

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KIIDs”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KIIDs can be obtained from www.am.miraeasset.eu/fund-literature/ . The Prospectus is available in English, French, German, and Danish, while the KIIDs are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KIID before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary/.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Hong Kong: This document is intended for Hong Kong investors. Before making any investment decision to invest in the Fund, Investors should read the Fund’s Prospectus and the information for Hong Kong investors (of applicable) of the Fund for details and the risk factors. The individual and Mirae Asset Global Investments (Hong Kong) Limited may hold the individual securities mentioned. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Copyright 2025. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.