THIS MATERIAL IS A MARKETING COMMUNICATION.

India’s Comeback Story – How, Why, and Where

India’s economy is slowing down. GDP growth for 2Q FY19/20 recorded at 4.5% – the lowest since 20131. In contrast, the country hit over 8% GDP growth for FY16/17. The government is also unlikely to achieve its fiscal deficit target.

These have sparked concerns about the health of the Indian economy. While understandable, they are overblown.

The India Story – Long-Term Growth versus Short-Term Headwinds

The Indian economy is facing a short-term slowdown. But its structural and fundamental factors should allow it to weather these near-term storms and thrive over the longer term. Its current headwinds are, as the World Bank2 notes, mostly driven by external and cyclical factors.

India’s Nominal GDP Growth Bottoming Out

Source: Bloomberg, November 2019

Meanwhile, country-specific issues are or have already been resolved – their impact has just yet to impact economic figures. Indeed, we expect further declines before an eventual bottoming out. Subsequently, India’s structural and economic fundamentals will come to the fore. These include a 37-year demographic dividend, a rising middle class, and ongoing government reforms.

Period of Demographic Dividend in Large Economies

But not all sectors will benefit equally. We will next study how these will affect each area of the market, beginning with the financial industry.

Unlocking the Potential of India’s Financial Sector

Four main structural challenges have hampered the realisation of the Indian financial industry’s potential. But as these are resolved, the sector (and economy) will stand poised for substantial long-term growth.

CHALLENGE #1: Disproportional State Dominance

State-owned banks hold almost 70% of sector assets3. Reducing this is thus a significant step toward a healthier system. This is being achieved through public-sector bank consolidation and bank licensing liberalisation. The number of state-owned banks is being cut from 27 to 124, while final guidelines for a new licensing regime were recently issued.

CHALLENGE #2: Persistent Asset Quality Issues

While non-performing assets (NPAs) continues to drag on the economy, the private sector has emerged mostly unscathed. The gross NPA ratio for private banks at the end of FY2019 was 3.7%5 compared to 12.6% for public sector banks. Public sector issues are also being resolved through asset-quality reviews, capital injections, regulations6, and write-offs7.

CHALLENGE #3: The Shadow Banking Liquidity Crunch

The 2018 default of India’s leading infrastructure finance company created a panic about liquidity in the NBFC (Non-Bank Financial Company) subsector – responsible for over 20% of system credit. But nothing happened beyond several isolated defaults. Their diverse business models shielded them from contagion effects. Further, the affected NBFCs and concerned loans only accounted for a tiny percentage of total system credit.

CHALLENGE #4: Low Financial Inclusion

Despite having 190 million unbanked adults in 20178, the government’s financial inclusion agenda has been highly successful. Its PMJDY initiative saw 377 million bank accounts opened from 2014 to 2019. The programme’s even more ambitious successor was launched in 2020.

As financial inclusion grows, Indians’ savings are also increasingly financialised9 and less physical. This development will have a deepening effect on capital markets.

Savings are Expected to Rise Sharply Going Ahead

Source: RBI, Kotak, Swiss Re, JP Morgan Research, Mirae Asset Global Investments

Mirae’s strategy

Mirae’s strategy is heavily weighted toward the financial sector. We focus on the disproportionate beneficiaries of sectoral reforms and the recovering economy: quality private sector banks, strong NBFCs, and large insurance companies (which will gain from higher financialisation).

Protection Gap is Large in India

The Evolution of the Indian Consumption Narrative

Domestic consumption already accounts for 60% of GDP. Trends within the consumption narrative thus play a huge role in the direction of the economy. Each of the following five trends will have positive implications for specific sectors such as consumer durables, consumer discretionary, real estate, and healthcare. Mirae Asset’s strategy is to carefully research and pick out the winners within those sectors.

TREND#1: Rising Incomes Concentrated Around the Middle Class

India is becoming a middle-class economy. From 2018 to 2030, India is expected to add about 140 million middle-class and 21 million high-income households while lifting 25 million households out of poverty.

India Households Growth

This growing wealth will lead to a premiumisation effect – the increased consumption of higher-quality goods, which will be reflected in higher spending on more nutritious food, better healthcare, modern appliances, and discretionary outlay.

TREND#2: The Continued Prevalence of a Younger, Tech-Savvy Demographic

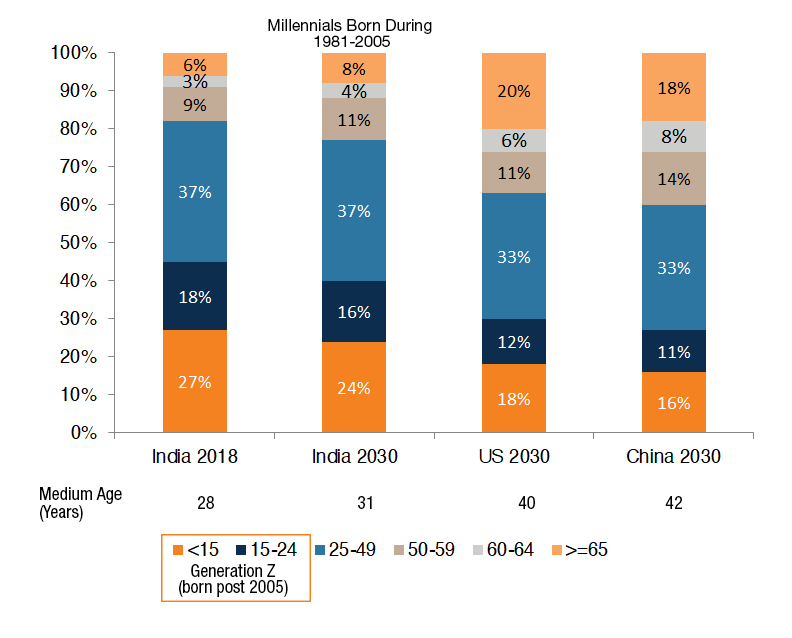

With its demographic dividend expected to last till 2055, India will be dominated by a young and tech-savvy generation. By 2030, millennials and Generation Z will comprise 77% of the total population. Generation Z will itself consist of 370 million people – ‘digital natives’ who will be accustomed to and even prefer technology-enabled consumption models.

Population by Age Cohort

Source: Euromonitor

TREND#3: Digital Influence on Consumer Habits

The Internet’s reach is becoming increasingly democratised. By 2030, an estimated 1.1 billion Indians will be online, supported by falling prices of data and smartphones. This premiumisation effect will thus influence the consumption patterns of even the lower-income classes.

Strong Growth in Digital Retail Transactions

Source: As of Oct 2019, Morgan Stanley Research

TREND#4: Greater Urbanisation and a Shrinking Urban-Rural Divide

India’s vast rural population creates massive long-term growth potential. By 2030, 40% of the population will be urban residents, primarily driven by the government’s ambitious infrastructure development projects. These moves will also aid industries with high logistical costs, such as mining, construction, agriculture, and FMCGs.

Sectors with High Logistics Costs to See Gains

Source: KPMG, BofA Merrill Lynch, June 2019

Consumer Expenditure in India Across City Types

Source: PRICE Projections based on ICE 360o Surveys (2014, 2016, 2018)

The gap between rural and urban population will also continue to shrink. From 2018 to 2030, per-capita consumption is forecast to grow by 3.5x for urban dwellers and 4.3x for rural ones. But the true potential of India’s rural population will be unlocked once the long-term catalyst of large-scale infrastructure development takes effect.

TREND#5: Increased Demand for Quality Healthcare Services

Rising incomes and premiumisation trends among the middle class and expanded access (the National Health Protection Scheme provides US$7,000/year to over 100 million families) will combine to boost healthcare demand. The growing incidences of lifestyle diseases will support the longer-term trend.

Your Vehicle for Investing in India’s Established and Future Sector Leaders

Once the Indian economy blows past its short-term headwinds, all signs point toward it continuing its path of steady long-term growth. But not all companies will benefit equally. Certain businesses will gain disproportionately. These are the companies the Mirae Asset India Sector Leader Equity Fund methodically identifies and invests in. For investors looking to leverage India’s long-term economic trajectory, our fund could be the perfect choice.

1 Reuters, as of 29 November 2019.

2 World Bank Group, as of Fall 2019.

3 Business Standard, as of 13 Oct 2019.

4 DB Research, Imagine 2030.

5 UNFPA, as of 31 Jan 2020.

6 The Economic Times, as of 22 Jul 2019.

7 World Economic Forum, Insight Report, January 2019.

8 Bain & Company, as of 8 January 2019.

9 Reuters, as of 28 August 2019.

Disclaimer

This material is neither an offer to sell nor solicitation to buy a security to any person in any jurisdiction where such solicitation, offer, purchase or sale would be unlawful under the laws of that jurisdiction. Investment involves risk.

The information in this material is based on sources we believe to be reliable but we do not guarantee the accuracy of completeness of the information provided. This material has not been reviewed by SFC and shall only be circulated in countries where it is permitted.

This material is intended solely for your private use and shall not be reproduced or recirculated either in whole or in part, without the written permission of Mirae Asset Global Investments. This document has been prepared for presentation, illustration and discussion purposes only and is not legally binding. Whilst compiled from sources Mirae Asset Global Investments believes to be accurate, no representation, warranty, assurance or implication to the accuracy, completeness or adequacy from defect of any kind is made. The division, group, subsidiary or affiliate of Mirae Asset Global Investments which produced this document shall not be liable to the recipient or controlling shareholders of the recipient resulting from its use. The views and information discussed or referred in this report are as of the date of publication, are subject to change and may not reflect the current views of the writer(s). The views expressed represent an assessment of market conditions at a specific point in time, are to be treated as opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. In addition, the opinions expressed are those of the writer(s) and may differ from those of other Mirae Asset Global Investments’ investment professionals.

The provision of this document shall not be deemed as constituting any offer, acceptance, or promise of any further contract or amendment to any contract which may exist between the parties. It should not be distributed to any other party except with the written consent of Mirae Asset Global Investments. Nothing herein contained shall be construed as granting the recipient whether directly or indirectly or by implication, any license or right, under any copy right or intellectual property rights to use the information herein. This document may include reference data from third-party sources and Mirae Asset Global Investments has not conducted any audit, validation, or verification of such data. Mirae Asset Global Investments accepts no liability for any loss or damage of any kind resulting out of the unauthorized use of this document. Investment involves risk. Past performance figures are not indicative of future performance. Forward-looking statements are not guarantees of performance. The information presented is not intended to provide specific investment advice. Please carefully read through the offering documents and seek independent professional advice before you make any investment decision. Products, services, and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries, and/or distributors of Mirae Asset Global Investments as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction.

Hong Kong: This material is prepared by Mirae Asset Global Investments (HK) Limited (Mirae HK). Mirae HK is regulated by the SFC (CE reference: ALK083).

United Kingdom: This document does not explain all the risks involved in investing in the Fund and therefore you should ensure that you read the Prospectus and the Key Investor Information Documents (“KIID”) which contain further information including the applicable risk warnings. The taxation position affecting UK investors is outlined in the Prospectus. The Prospectus and KIID for the Fund are available free of charge from http://investments.miraeasset.eu, or from Mirae Asset Global Investments (UK) Ltd., 4th Floor, 4-6 Royal Exchange Buildings, London EC3V 3NL, United Kingdom, telephone +44 (0)20 7715 9900.

This document has been approved for issue in the United Kingdom by Mirae Asset Global Investments (UK) Ltd, a company incorporated in England & Wales with registered number 06044802, and having its registered office at 4th Floor, 4-6 Royal Exchange Buildings, London EC3V 3NL, United Kingdom. Mirae Asset Global Investments (UK) Ltd. is authorised and regulated by the Financial Conduct Authority with firm reference number 467535.

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KIIDs”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KIIDs can be obtained from www.am.miraeasset.eu/fund-literature/ . The Prospectus is available in English, French, German, and Danish, while the KIIDs are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KIID before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary/.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Hong Kong: This document is intended for Hong Kong investors. Before making any investment decision to invest in the Fund, Investors should read the Fund’s Prospectus and the information for Hong Kong investors (of applicable) of the Fund for details and the risk factors. The individual and Mirae Asset Global Investments (Hong Kong) Limited may hold the individual securities mentioned. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Copyright 2025. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.